From experimentation to execution across Africa’s insurtech landscape.

Across Africa, the insurance innovation conversation is shifting in measurable ways. Early experimentation is giving way to structured regulatory engagement, partnership-driven distribution, and capital mobilisation aligned to inclusive resilience objectives. This transition reflects a maturing ecosystem where startups, insurers, regulators, and investors are increasingly working in coordinated rather than parallel pathways.

This newsletter edition highlights ecosystem progress through three lenses: institutional momentum, startup venture execution, and regulatory advancement. Together, these developments illustrate how practical learning, supervisory openness, and market collaboration are collectively shaping the next phase of insurtech growth across the continent.

Regulatory Momentum: Zambia and Zimbabwe advance sandbox pathways

Zambia and Zimbabwe

Recent regulatory progress in Zambia and Zimbabwe marks an important institutional shift toward adaptive supervision models that enable controlled innovation testing.

Zambia’s Pensions and Insurance Authority (PIA) announced the rollout of a dedicated insurance regulatory sandbox, creating an environment in which insurers and innovators can test products and technologies under supervision while maintaining policyholder safeguards.

The framework reflects broader regulatory modernisation efforts aimed at balancing innovation enablement with consumer protection. You can read the PIA sandbox guidelines here.

Zimbabwe’s Insurance and Pensions Commission (IPEC) similarly advanced its sandbox platform, allowing insurers, startups, and intermediaries to pilot new solutions within defined regulatory parameters before full market deployment. This structure provides clear monitoring, evaluation, and exit pathways that support iterative refinement while limiting systemic risk. You can review the IPEC sandbox guidelines here.

These developments are significant because they reflect regulators moving beyond compliance enforcement toward collaborative innovation oversight. Sandboxes reduce uncertainty around product classification, licensing pathways, and supervisory expectations while allowing regulators to gain visibility into emerging business models.

For insurers and innovators alike, this lowers friction between experimentation and deployment and strengthens regulator-industry dialogue across markets.

Regulatory readiness is becoming a shared institutional objective. Sandboxes signal a transition from static rule application toward supervisory partnership models that materially accelerate responsible innovation.

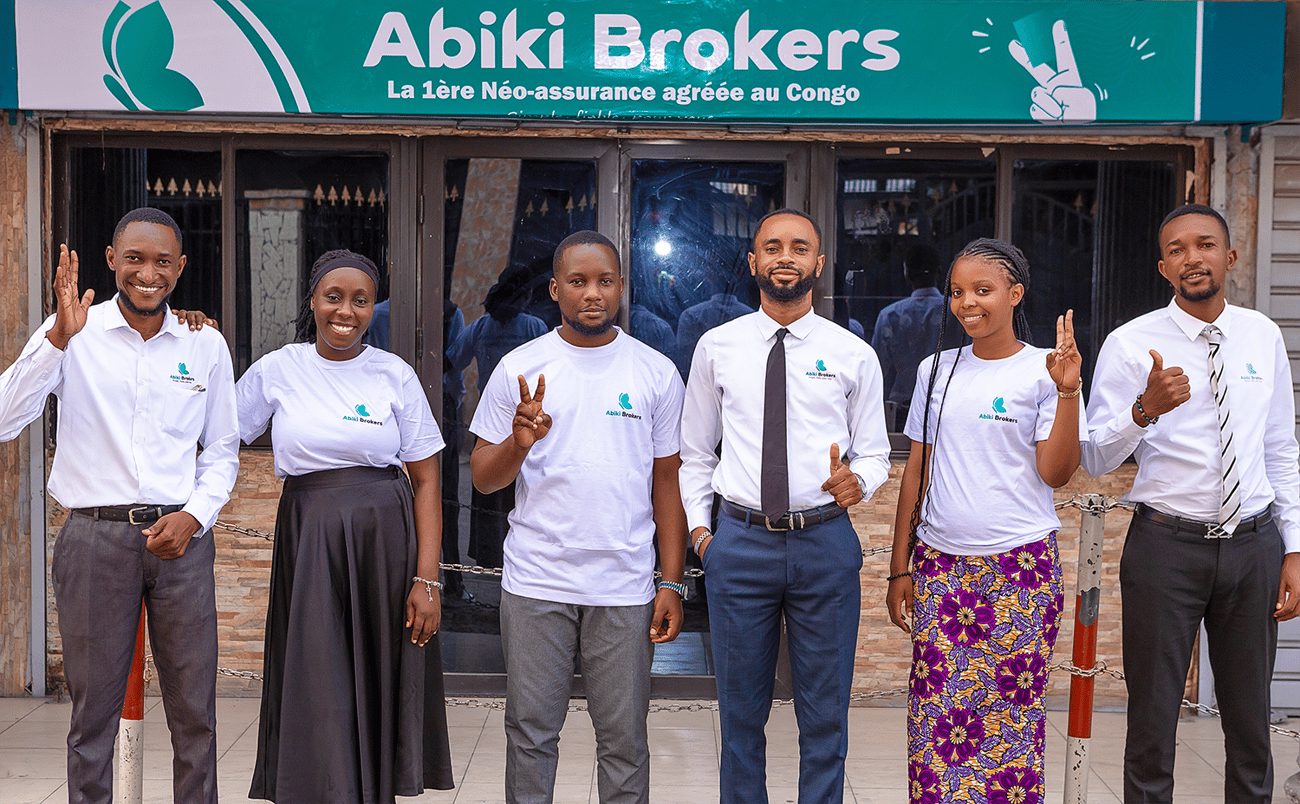

Abiki Brokers: Regulatory capability translating into market participation

Democratic Republic of Congo

Across many African markets, expanding insurance access is not only about designing new products but also about solving distribution challenges. In the Republic of Congo, where more than 90 percent of the working population remains uninsured, informal workers and small businesses are often exposed to financial shocks such as accidents, transport disruptions, or credit loss without any form of protection.

Abiki Brokers is addressing this gap by building an embedded insurance infrastructure that integrates protection directly into everyday financial and commercial services. Rather than requiring customers to actively purchase insurance, the model embeds coverage into existing transactions through partner platforms. Insurance is therefore included at the point of use, supported by low premiums, digital payment channels, and automated subscription processes that simplify onboarding and policy management.

Licensed in the Republic of Congo by the Directorate General of National Financial Institutions under the Ministry of Finance, Abiki operates as a technology-enabled microinsurance platform designed for scale. Its digital infrastructure supports simplified subscription, automated policy administration, claims management, and reporting while integrating payment channels such as mobile money and card-based systems. This technology is designed specifically for high-volume distribution through partner ecosystems rather than traditional retail insurance channels.

Traditional insurance channels have struggled to reach these segments due to cost, limited distribution networks, and complex customer journeys. The company’s product portfolio focuses on everyday protection needs delivered through embedded models. Key offerings include credit insurance distributed through craftsmen networks, credit sales providers, and microfinance institutions; accident and death insurance linked to transportation and professional activities; and flexible micro-cover products designed for frequent use scenarios. These products are structured around recurring low-premium payments and high-volume distribution partnerships.

Abiki has already established early traction through strategic partnerships that enable large-scale distribution. Premium payments are supported through Mobile Money Congo, while collaboration with ONYFAST integrates prepaid cards with embedded insurance solutions. Through engagement with the Ministry of Small and Medium Enterprises and Craftsmanship, the company has developed credit insurance solutions targeting more than 18,000 artisans, while its ONYFAST partnership connects to a user ecosystem of over 41,000 customers.

These partnerships form part of a broader distribution pipeline that includes microfinance institutions, interurban transport networks, travel agencies, and consumer credit providers. This ecosystem approach allows Abiki to reach customers through services they already use, significantly reducing customer acquisition costs while enabling rapid scale.

The company’s business model is built around recurring insurance premiums delivered through business-to-business and business-to-business-to-consumer partnerships. Automated processes reduce operational costs while volume-based distribution improves margins over time. The model is designed to remain locally profitable while maintaining affordability for customers.

Abiki Brokers was also selected for and successfully completed the BimaLab Africa InsurTech acceleration programme, strengthening its platform capabilities and partnership strategy. Looking ahead, the company aims to expand product deployment across additional partner networks, targeting 30,000 active insured customers in the near term and scaling toward more than 100,000 insured users within the next two years.

Abiki Brokers illustrates how embedded insurance models can unlock access in markets where traditional distribution has struggled to reach large segments of the population. By integrating insurance directly into financial services, transport systems, and commercial platforms, the company demonstrates how technology-enabled partnerships can extend protection to informal workers and underserved communities while supporting broader financial resilience.

ACRE Africa: Scaling Climate Resilience and Inclusive Protection Across Agricultural Markets

Across many African agricultural economies, insurance is increasingly becoming more than a financial product. It is emerging as an enabling tool that helps farmers manage climate uncertainty, stabilise livelihoods, and adopt more sustainable production practices. Recent milestones from ACRE Africa illustrate how partnerships, capital investment, and product innovation are converging to expand resilience for smallholder communities across the continent.

This momentum is reflected in growing recognition that insurance can act as a protective shield against climate shocks. Coverage and bundled risk solutions have been shown to help farmers maintain productivity and avoid severe income loss when extreme weather disrupts harvest cycles. At the same time, access to structured protection mechanisms is encouraging uptake of improved farming practices, as reduced risk exposure allows producers to invest more confidently in climate-smart inputs and technologies.

These developments underscore why insurance is increasingly being viewed not as a peripheral service, but as a core component of agricultural sustainability and financial inclusion frameworks. Against this backdrop, ACRE Africa strengthened its operational capacity in 2025 through targeted investment and commercial engagement. An equity investment by TAN RE into its Tanzanian operations reinforced capitalization and long-term market positioning.

Complementing this, a CGIAR Scaling for Impact grant supported expansion of digital financial service tools such as climate scoring and agricultural risk assessment systems designed to foster technology adoption among smallholder farmers. ACRE also secured a commercial tender with NIC Tanzania, signalling continued demand for structured agricultural protection services within the market.

Building on this foundation, partnership activity expanded delivery reach and institutional collaboration. An agreement with MUA Insurance enabled the rollout of Index-Based Livestock Insurance across multiple Tanzanian regions, strengthening climate risk protection for pastoralist communities whose livelihoods depend heavily on environmental stability. Concurrently, a multi-year collaboration with CRDB Bank is advancing sector capability through training programmes focused on insurance literacy and financial inclusion. At a strategic level, cooperation with ZEP-RE PTA Reinsurance and the Grameen Crédit Agricole Foundation is supporting inclusive agricultural finance initiatives designed to de-risk lending environments and improve credit access for smallholder farmers.

These partnership-driven efforts reflect a broader ecosystem trend where insurance is increasingly embedded within financial service delivery rather than offered in isolation. Bundled models linking credit, inputs, and protection are demonstrating effectiveness in safeguarding livelihoods while enhancing market participation. Such approaches also show promise in addressing protection gaps among women farmers and underserved groups by integrating insurance into services already used within local economic structures.

Product innovation during the year reinforced this trajectory. A climate resilience insurance solution launched in Kenya through collaboration with insurers, development partners, and microfinance actors targeted large-scale farmer inclusion during seasonal rollout. In Zambia, a pilot initiative exploring mutual insurance structures within savings groups is testing mechanisms to formalise community-based protection models while preserving ownership and flexibility for members. These initiatives highlight a growing shift toward locally adaptive models that align formal insurance structures with existing community financial practices.

Geographic expansion further extended impact, with operations entering additional African markets including Central and Southern African jurisdictions. Expansion of parametric and index-based solutions into new environments reflects increasing demand for scalable approaches that respond quickly to climate variability. This progression signals a transition from pilot deployments toward regional platforms capable of delivering protection across diverse agricultural systems.

Collectively, these developments contribute to measurable reach. ACRE Africa’s programmes have now impacted millions of farmers continent-wide, with substantial numbers accessing crop and livestock protection services during 2025 alone. Such a scale reinforces the growing role of agricultural insurance in stabilising production systems and strengthening resilience against climate volatility.

ACRE Africa’s progress illustrates an important structural shift within inclusive insurance ecosystems. Advancement is increasingly driven by coordinated collaboration linking insurers, reinsurers, financial institutions, development partners, and technology providers. Insurance is no longer operating as a standalone intervention. Instead, it is being embedded within broader frameworks that address finance access, sustainability incentives, and climate adaptation outcomes simultaneously.

As climate variability intensifies and agricultural markets evolve, solutions built on integrated partnerships and locally responsive design will remain central to narrowing protection gaps. The trajectory observed across ACRE Africa’s activities reflects how collaborative models can move beyond experimentation toward durable resilience outcomes that support both livelihoods and long-term sector stability.

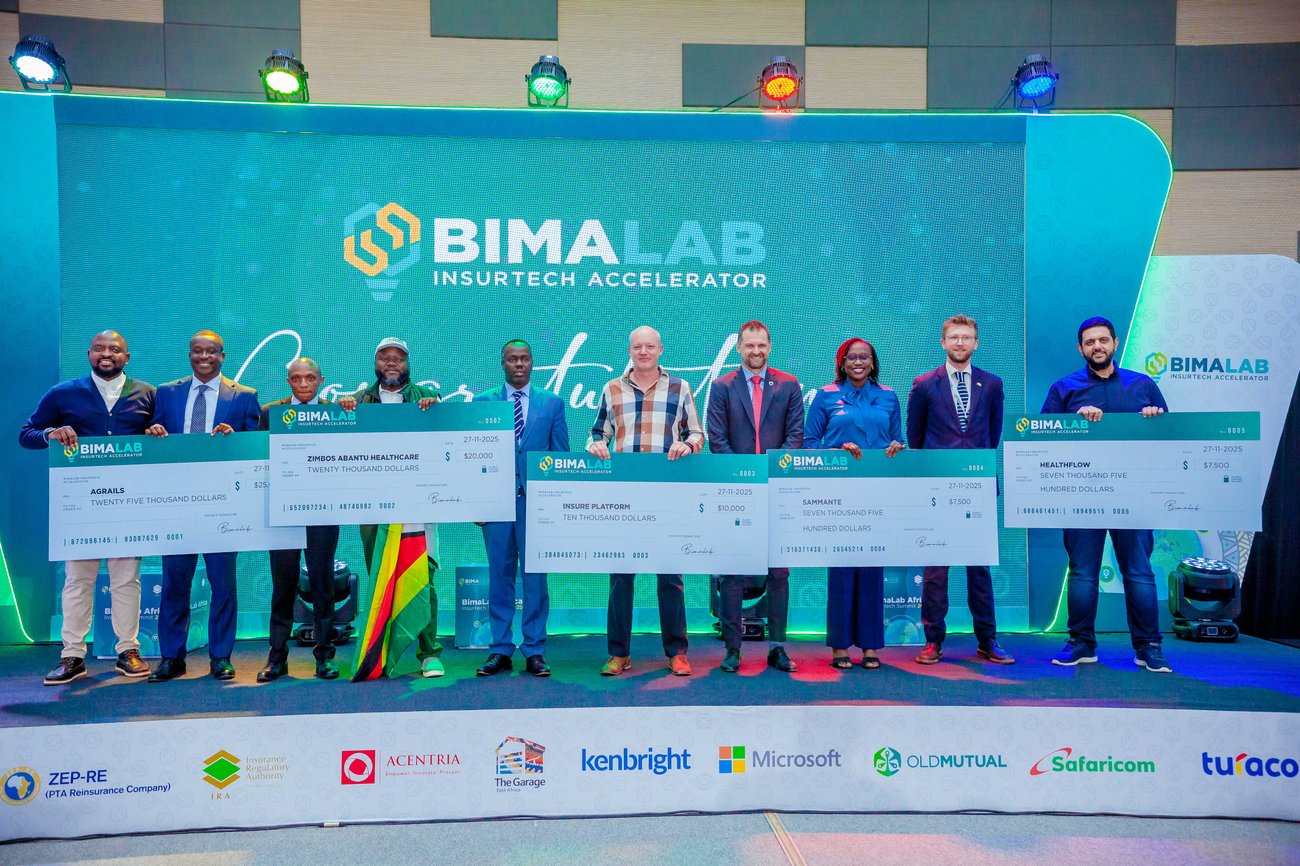

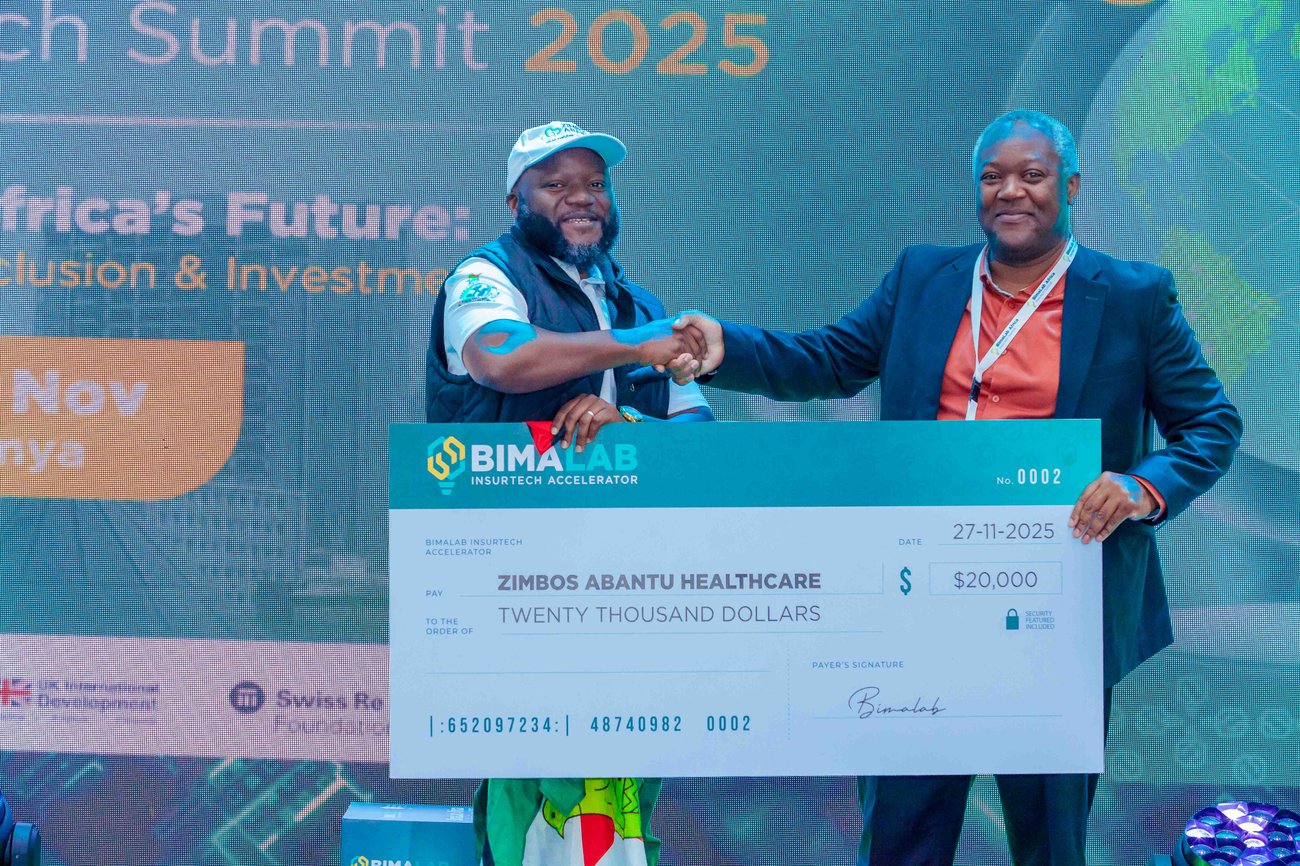

ZimbosAbantu Healthcare: Relationship capital enabling regional expansion

Zambia

ZimbosAbantu Healthcare entered structured partnership discussions with Sanlam Zambia, reflecting a progression from domestic traction toward cross-border opportunity.

The expansion pathway was deliberately sequenced. Rather than prioritising rapid entry, the venture focused on relationship-building, insurer alignment, and internal readiness.

Product assumptions were stress-tested for the target market; governance practices were strengthened, and reporting processes refined.

This preparation shifted engagement dynamics from exploratory dialogue to pilot-level discussions grounded in execution feasibility. The case illustrates how ecosystem convenings such as the BimaLab Africa Innovation for Resilience Summit in Zambia, 2025 and mentorship can convert introductions into tangible collaboration.

Regional scale is achieved through preparation and alignment rather than acceleration alone. Trust-based ecosystem linkages materially increase expansion of success probability.

From local validation to regional scale: ZimbosAbantu Healthcare

Zambia

ZimbosAbantu Healthcare’s expansion journey offers a useful illustration of how ecosystem infrastructure supports venture progression beyond early traction.

The venture demonstrated strong early adoption in its domestic market, positioning itself to explore regional opportunities. However, cross-border expansion introduced regulatory variability, partnership complexity, and operational risk. Without structured preparation, scaling prematurely could have exposed the organisation to strategic misalignment or reputational risk.

Through BimaLab’s ecosystem convening in Zambia in October 2025, the venture engaged regional insurers in structured dialogue environments designed to explore collaboration rather than pitch products. Mentorship supported internal readiness evaluation, highlighting gaps in reporting structure, governance clarity, and market positioning.

Rather than pursuing parallel expansion, leadership recalibrated strategy to prioritise depth of preparation. Product assumptions were localised, data practices strengthened, and operational workflows aligned with partner expectations.

Engagements evolved into pilot exploration discussions grounded in execution of viability. Expansion conversations transitioned from conceptual to implementable, improving collaboration credibility and reducing partnership risk.

Many ventures struggle during transition from local validation to regional scale. This case demonstrates that ecosystem support focused on readiness rather than acceleration can materially improve expansion quality and sustainability.

The BimaLab convening series represented a central ecosystem milestone, functioning not simply as programme events but as infrastructure enabling collaboration across fragmented markets

PARTICIPATION & REACH

The BimaLab Africa Insurtech Summit convened over 400 delegates from more than 20 countries alongside speakers, venture showcases, workshops, and immersion visits. Broader Summit and Demo Day activities engaged industry leaders, regulators, and founders across multiple structured sessions.

Executive dialogue sessions brought together senior insurance leaders, while startup showcases and breakout sessions enabled deeper partnership engagement. These participation levels reflect increasing ecosystem density and institutional interest in insurtech development.

KEY DEVELOPMENTS DURING THE SUMMIT

🔹 Market immersion for ventures: Curated field engagements enabled founders to test commercial assumptions directly with market actors, refining pricing logic, distribution understanding, and value articulation through real feedback.

🔹 Capital ecosystem signalling: The announcement of the inclusive insurtech investment fund, 3IF, a major inclusive insurtech investment initiative during the convening signalled institutional confidence and strengthened investment pathways for emerging ventures. This first of its kind fund is backed by FSD Africa investments with initial investment from ZEP-RE.

🔹 Executive alignment dialogue with Insurance Company CEOs in Kenya: Closed-door discussions with insurance leaders allowed candid and intimate engagement on sector barriers and collaboration models with insurtechs and opportunities for the insurance industry in Kenya to collaborate on FSD Africa initiatives such as 3IF and MICA (Mobilising Insurance Capital for Green Investments in Africa), strengthening strategic relationship infrastructure.

🔹 Venture positioning: Themed showcase sessions throughout the summit enabled startups to present validated models to investors and insurers, accelerating movement toward partnership and capital engagement. As innovation ecosystems mature, these gatherings shift from being about visibility to becoming spaces where real coordination and collaboration take place.

You are receiving this email because you are part of our contact database. If you don't recognise this, or you would like to stop receiving emails from FSD Africa, you can unsubscribe by simply clicking on the button below.